Fighting Energy Market Volatility Without a Risk Desk?

You're not alone. PowerNavigator is the AI-powered platform designed for companies like yours, empowering you with the tools to hedge against price risks and to optimize procurement like a major player.

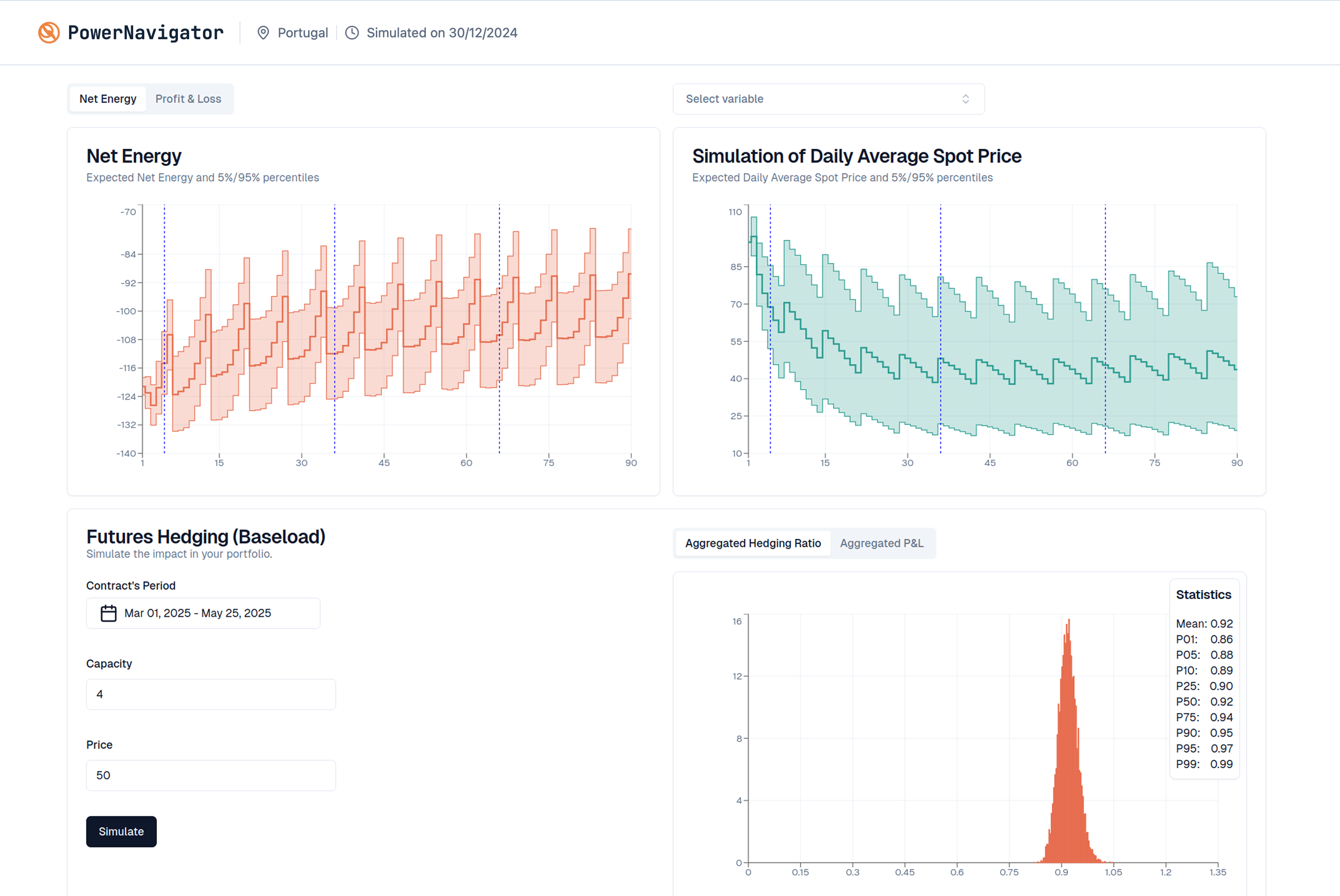

Get to know PowerNavigator

Full Probability Distributions

Understand all possible outcomes for price, grid load, renewables generation and their chances with full probability distributions, not just averages.

Custom Forecasts

We can provide custom forecasts specific to your consumption or production data and integrate it to PowerNavigator

Easy to Use Dashboard & API

Flexible data access via API or easy-to-use dashboards, fitting your existing workflows.

Why Choose Us

Built for Energy Challenges

Proprietary AI Models Tailored for Volatile Energy Markets

For Teams Without a Risk Desk

Designed for Smaller Companies & Industrial Consumers

Always Up to Date

Continuous Model Updates Backed by Research

Full Probability Distribution

Accurate, probabilistic insights that go beyond averages

FAQ

Turn Energy Volatility into Your Advantage

PowerNavigator provides the foresight to make smarter energy trading and procurement decisions, driving down costs and maximizing returns.